6.0 What the four zones are and what they are not

You have two numbers from Sections 4 and 5: an ORS value and an MTS value. Their sum is your HERI-40 total score on a scale from 0 to 200. The section that follows answers the one question that has to come at this point. What does the score mean concretely, who pays for a chain at that level, and what negotiating position does it put you in.

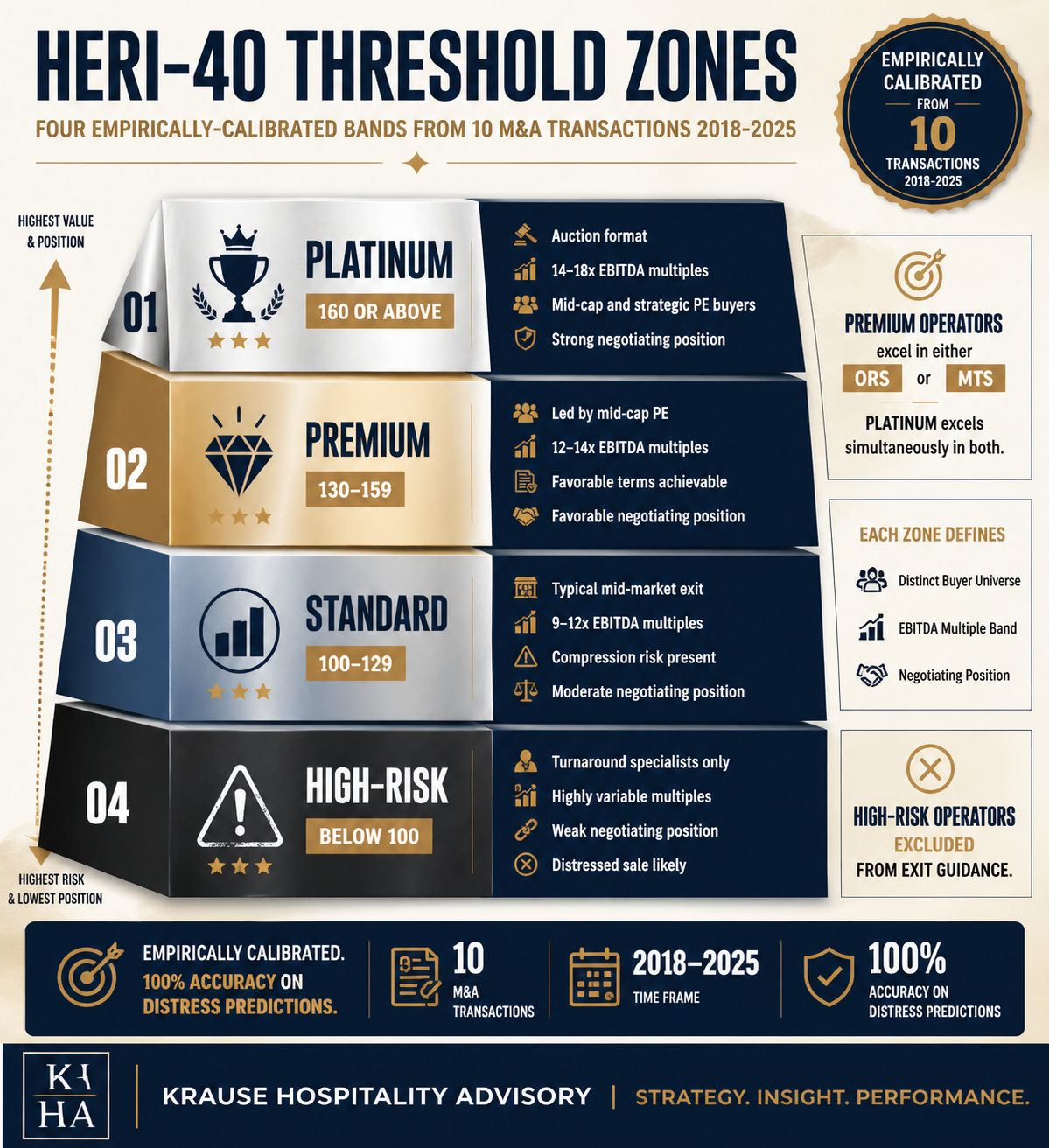

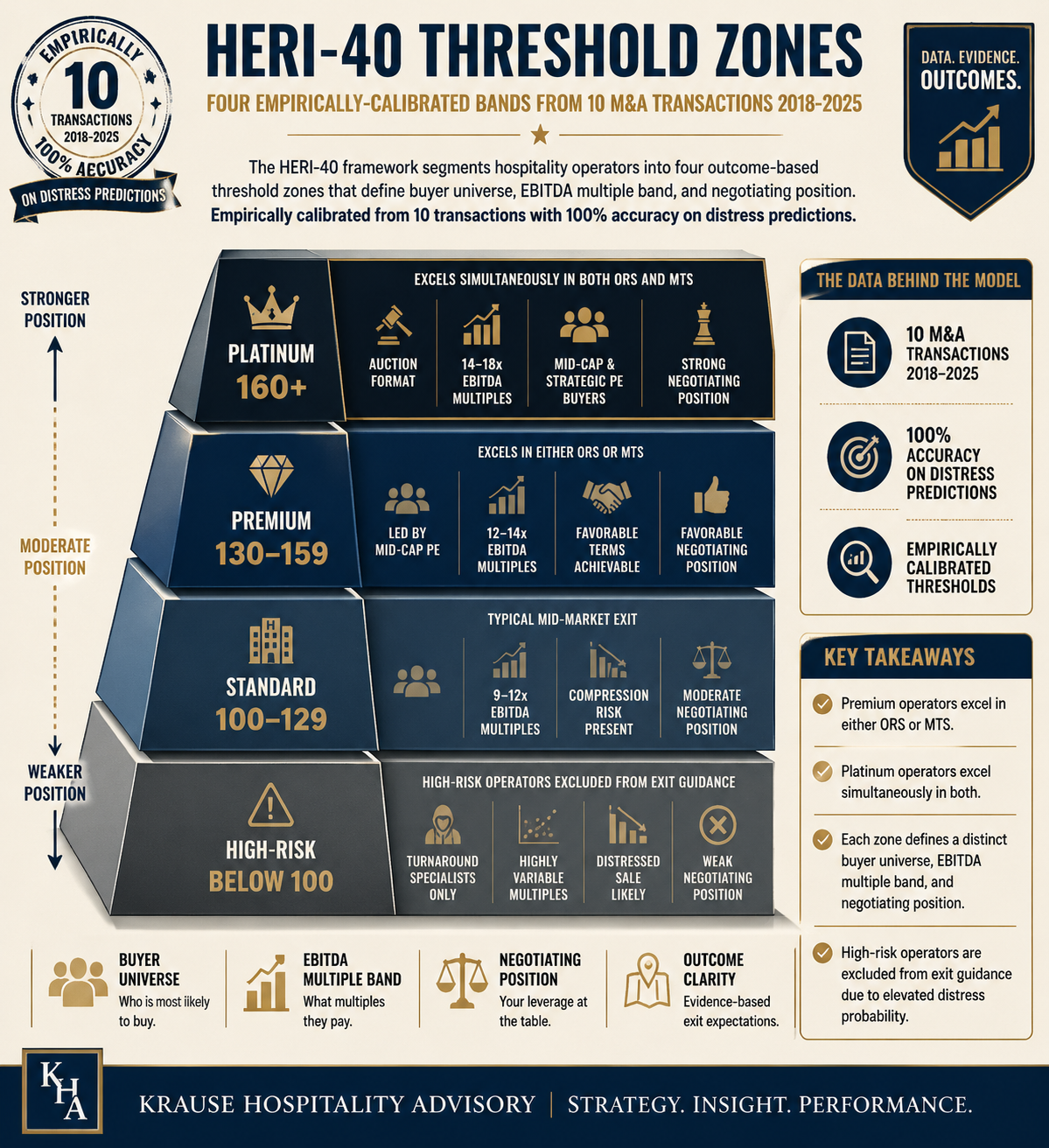

The answer falls into four zones. Platinum from a score of 160, Premium 130 to 159, Standard 100 to 129, High-Risk below 100. The three thresholds are not arbitrary terciles. They come out of the retrograde backtest documented in full in Appendix A: ten historical hospitality transactions from the 2018–2025 window were run against the framework and the realised EBITDA multiples were compared with the reconstructed HERI-40 scores. The empirically observed buyer segments and multiple bandwidths cluster precisely at those three thresholds. 100 separates continuable trades from distress paths, 130 separates mid-market zones from strategic buyer demand, 160 separates frequent premium exits from rare platinum auctions.

One disclaimer before stepping into the zones themselves: zones are indications, not verdicts. A Premium score without a strategic buyer still sits on the market. A Standard score with a synergetic acquisition story can realise a Premium multiple in auction. The number orders probabilities. It does not replace buyer analysis, broker work, or due diligence. What it does: it calibrates expectations before the sale process begins, and it makes the chain's own weak points visible before a buyer finds them.

6.1 Platinum zone (score ≥ 160): the rare case

A Platinum score is empirically rare. In the documented backtest fewer than ten percent of multi-unit operators reach this level. Those who do sell into a different dynamic than the rest of the industry.

Buyer side: active are strategic acquirers with an established hospitality portfolio (Restaurant Brands International, Inspire Brands, Roark Capital as platform holding) along with large-cap private equity sponsors with their own hospitality track record. Auction format is the rule, not the exception. Two to four qualified bidders compete, often in mixed buyer structures combining strategics and financial sponsors.

Multiple bandwidth: fourteen to eighteen times EBITDA as the typical median bandwidth of the Platinum zone. That is a premium of roughly forty percent over the industry median of the mid-market. The two backtest anchors from Appendix A mark the upper leading edge of the zone and sit noticeably above the median. Dutch Bros went public in 2021 with a reconstructed score of 181 to 184; the deal multiple on post-IPO trailing EBITDA sat above 30 times. Jersey Mike's was taken private by Blackstone in 2024, score 181 to 183, multiple on reported EBITDA around 24 to 26 times (deal value approximately USD 8 billion). Hypergrowth IPO candidates and marquee auction processes regularly deliver scarcity-premium multiples above the median bandwidth — the median describes the typical Platinum transaction, not its peak. Both anchor deals share three structural features: unit economics well above industry median, system maturity of more than eight years of continuous growth, whitespace runway above fifty percent of the addressable market.

Negotiating position: in the Platinum zone the seller selects the buyer. Earn-out constructions are short or absent, roll-over equity is optional rather than forced, management lock-ups are symbolic rather than binding. Purchase price is often structured as cash plus a small earn-out tranche, not as a proceeds split over several years.

Strategic implication: a Platinum position keeps three paths open. First, a trade to a strategic acquirer with a full takeover. Second, a partial exit via a minority stake to a large-cap sponsor with ongoing owner participation. Third, IPO given the right market window and size threshold (usually from EUR 300 million in revenue). All three paths are open. The question is not whether, but which valuation logic the seller wants to maximise.

6.2 Premium zone (score 130 to 159): the strategic target zone

The Premium zone is the zone at which most well-run multi-unit operators in DACH and the broader EU can realistically aim. A score between 130 and 159 signals to buyers: fully continuable, strategically interesting, not extraordinary, but institutionally carryable.

Buyer side: active are mid-cap private equity sponsors with buy-and-build theses (in DACH and the EU for example Triton, Ardian, EQT Mid Market, IK Partners), strategic acquirers with geographic or concept fit (regional expansion of a larger chain, completion of a missing segment position in a portfolio), and in individual cases an IPO at the upper threshold from a score of 150. Two to four qualified bidders are realistic, auction-like structures are possible but not the norm. The classic structure is an exclusive or semi-exclusive process with one or two preference bidders and a structured backup path.

Multiple bandwidth: twelve to fourteen times EBITDA as the typical median bandwidth of the Premium zone. The two backtest anchors from Appendix A sit above this median and illustrate the upper end of the zone. L'Osteria was acquired by the McWin platform in 2023, reconstructed score between 153 and 162 depending on the sub-segment multiples reference date, EBITDA multiple in the 15 to 18 times range. Firehouse Subs was acquired by Restaurant Brands International in 2021, score between 152 and 172 depending on the MTS reference date within that hot QSR acquisition year, multiple roughly 20 times (deal value USD 1 billion on roughly USD 50 million EBITDA). Leading deals with either ORS or MTS premium drivers — as laid out for L'Osteria and Firehouse Subs in the paragraph immediately below — regularly achieve multiples above the median bandwidth.

An important differentiation against the Standard zone directly below: Premium scores typically carry either an ORS premium driver or an MTS premium driver. Rarely both simultaneously. L'Osteria sat clearly in ORS-premium territory around 84 through high flow-through margin, consistent system maturity, and clean management depth, while the MTS sat at 73 to 78 under EU macro headwinds. Firehouse Subs was the inverse. ORS in the mid-range around 69 to 78, but MTS at 94 in the peak year of the US QSR acquisition market. Both patterns reach Premium level. The rare combination of high ORS and high MTS is what lifts a chain into the Platinum zone.

Negotiating position: you can shape terms. Earn-out length, roll-over equity share, management continuity, board governance are points of negotiation where you retain leverage. A price dictation against the buyer is not the rule, but in structured processes with multiple bidders a price span of one to two multiple points develops.

Strategic implication: a Premium score without strategic buyer fit typically leads to a mid-cap PE exit with a four- to six-year buy-and-build horizon. A Premium score with strategic fit lifts into the Premium-to-Premium uplift and can mobilise an additional one to two multiple points. Targeted preparation for strategic fit candidates, not only financial sponsors, is the most important lever in the final twelve months before a Premium exit. Which concrete levers work here is sketched in Section 8.

6.3 Standard zone (score 100 to 129): the mid-market home

The Standard zone is realistically reachable for the largest share of established multi-unit operators in DACH and the broader EU. It describes the mid-market exit: a trade is feasible, buyers are present, but terms shift in favour of the buy side.

Buyer side: active are lower-mid-cap private equity sponsors (in DACH for example Capvis, Castik, EMZ Partners; across the EU among others IK Partners at the Tier-2 level, Astorg on mid-cap positions), strategic roll-up acquirers with a synergy story around procurement, technology, or shared management layer. Rare: IPO (only with a clear growth story and minimum revenue), large-cap PE (only with strategic platform fit inside an existing buy-and-build programme).

Multiple bandwidth: nine to twelve times EBITDA. Two backtest anchors from Appendix A illustrate the zone. Del Taco was acquired by Jack in the Box in 2022, reconstructed score between 121 and 136 depending on the sub-segment reference date, synergy-adjusted multiple around 7.6 times. What is particularly instructive about this deal is the subsequent re-divestiture in 2025 for USD 115 million, compared with the original USD 575 million in 2022. The trajectory retroactively confirms the zone classification. Del Taco stayed in the Standard zone and, without a clear premium driver, drifted further down between signing and refranchising. The second anchor is Subway, taken private by Roark Capital in 2023, score between 127 and 142 depending on how whole-business-securitisation financing is treated inside operating EBITDA. Subway is an edge case at the Premium boundary; the detailed explanation sits in Section 6.5 and in Appendix A.

Negotiating position: in the Standard zone the buyer dictates more often than the seller. Earn-out maturities of two to three years are standard, roll-over equity shares between twenty and forty percent are common, management lock-ups are enforced. Price latitude is not generated through bidder competition but through the quality of the equity story that makes subsequent value creation plausible to the buyer.

An important warning from the backtest: the Standard zone carries its own valuation-correction risk that no other zone carries to the same degree. Due-diligence periods of six to nine months are typical in this segment. Over those months the score can deteriorate, through falling like-for-like revenue, management departures, margin pressure in individual sub-segments. A Standard score of 125 at signing that slides to 115 by closing typically triggers renegotiations on purchase-price adjustments. The Del Taco sequence is the archetypal illustration of this risk.

Strategic implication: operators in the Standard zone have two paths. First, the deliberate development of premium drivers in the twelve to eighteen months ahead of a planned exit, in order to rise into the Premium zone. Second, the conscious acceptance of the mid-market exit with a realistic multiple target and a focus on deal structuring (cash at close, earn-out mechanics, roll-over terms). Section 8 supplies the 12-month roadmap by zone starting position.

6.4 High-Risk zone (score below 100): distress and triage

The High-Risk zone is not an exit zone in the institutional sense. A HERI-40 score below 100 signals that the combination of operational maturity and market window is so weak that regular buyer competition no longer forms.

Buyer side: active are turnaround-specialist private equity sponsors (for example Quantum Capital, OpCapita, Aurelius Equity Opportunities), distress specialists, occasionally former sponsors in rescue tranches. Strategic acquirers only appear in asset-cherry-picking mode: individual premium-location sites, the brand itself, the franchise pipeline as a platform asset. A full corporate sale to a strategic acquirer is the exception in this zone, not the rule.

Multiple bandwidth: four to eight times EBITDA on adjusted figures, where an EBITDA multiple is applicable at all. Typically the alternative realisation logic prevails: insolvency proceedings with asset sales (Vapiano 2020), Chapter 11 filing with creditor settlement (BurgerFi Q1 2024, Chapter 11 opening in September of the same year).

Negotiating position: none. In the High-Risk zone time works against the seller. Liquidity pressure, supplier tightening, staff departures, covenant breaches accumulate inside a few quarters. The buyer dictates price, structure, and timing.

Backtest anchors from Appendix A: BurgerFi, with a reconstructed score between 55 and 64 in Q1 2024, shows the classic High-Risk signature with negative flow-through trajectory, eroding unit-EBITDA dispersion, and an IPO market de facto closed to unprofitable chains. Vapiano, with a score between 35 and 65 across different sub-segment reference points, ended in the 2020 insolvency, with the remaining assets sold in piecemeal realisation. A classical EBITDA multiple was not generated.

An explicit methodological boundary at this point: operators in the High-Risk zone are not addressed in this paper via a HERI-40-based exit path. The methodology is built for trade preparation and zone improvement, not for distress restructuring. An operator in this zone needs restructuring specialists, possibly a Chief Restructuring Officer mandate, and work on the capital structure that sits outside the reach of this framework. That self-limitation is chosen deliberately and is to be read as methodological integrity.

6.5 Edge cases: zone boundaries and moving thresholds

Three case classes deserve separate mention because they refine the zone reading.

Zone-boundary operators. A score of 128 to 131 (Standard-to-Premium transition) or 158 to 162 (Premium-to-Platinum transition) has to be read in trend context, not as a static point value. A 131 score that has grown over twelve months from a 120 score sends a strategically different signal to buyers than a 131 score that has slipped from a 140 score. Trend direction is often weightier in the buyer conversation than the snapshot.

Whole-business-securitisation operators (Subway type). A score between 127 and 142, depending on how the WBS financing is treated inside operating EBITDA, marks an edge case at the Premium boundary. The WBS structure creates cash-pool flexibility that lifts operational room for manoeuvre above the Standard level. At the same time the governance overhead of the WBS structure enforces restrictions that block a rise into the true Premium zone. Subway is the archetypal illustration of this pattern. Details sit in Section 2.4 and in Appendix A.

ORS-strong-MTS-weak versus ORS-weak-MTS-strong. A HERI-40 score of 125 with an ORS-MTS split of 80 to 45 behaves structurally differently in the buyer conversation from a score of 125 with a 55 to 70 split. The first signature describes a Premium-ready operator waiting for a better market window. The second describes a mid-market-ready operator actively using a hot buyer window. Both strategies are coherent but lead to different timelines and different buyer target groups.

6.6 Transition to Section 7

Your score is calculated, your zone determined, the active buyer types and multiple bandwidths understood. Section 7 walks the full step-by-step calculation through the worked example L'Osteria: from the raw data set drawn from public sources and McWin press releases, through the individual scores A1 to A5 and B1 to B4, to the ORS and MTS sums, all the way to the final HERI-40 score in the Premium band between 153 and 162. Section 8 then delivers the 12-month roadmap by zone, with concrete levers that make zone improvement realistic inside that horizon.

Related research

- HERI-40 Section 1: Executive Summary

- HERI-40 Section 2: Market Context 2026

- The roll-up playbook in European hospitality: where multiple arbitrage still works

- Multiple compression in mid-market foodservice: reading the 2024–2025 corridor